FIS: Fundamental Ratio Analysis - Fidelity National Information Services Inc

FIS: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 18, 2026 a 03:43 pm

Consumer Staples Comparison. 18 Jul

Comparison of Consumer Staples. Where is strength and weakness? What has developed well and badly?

July 18, 2026 a 03:31 pm

WTW: Fibunacci Level Technical Analysis - Willis Towers Watson Public Limited Company

WTW: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 18, 2026 a 03:15 pm

LYB: Trend with Support and Resistance Levels - LyondellBasell Industries NV

LYB: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 18, 2026 a 02:03 pm

SPG: Analysts Ratings - Simon Property Group Inc

SPG: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 18, 2026 a 01:00 pm

DDOG: Fundamental Ratio Analysis - Datadog Inc

DDOG: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 18, 2026 a 01:00 pm

NVDA: Dividend Analysis - NVIDIA Corporation

NVDA: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 18, 2026 a 12:46 pm

AVB: Fundamental Ratio Analysis - AvalonBay Communities Inc

July 18, 2026 a 06:00 pm

WDAY: Analysts Ratings - Workday Inc

July 18, 2026 a 05:00 pm

IRM: Fibunacci Level Technical Analysis - Iron Mountain Incorporated

July 18, 2026 a 04:44 pm

IEX: Analysts Ratings - IDEX Corporation

July 18, 2026 a 04:38 pm

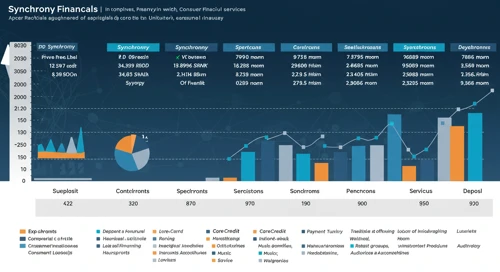

SYF: Analysts Ratings - Synchrony Financial

SYF: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 18, 2026 a 12:38 pm

Crypto Comparison. 18 Jul

Comparison of Crypto. Where is strength and weakness? What has developed well and badly?

July 18, 2026 a 12:31 pm

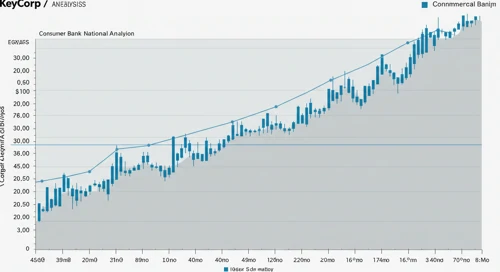

KEY: Fibunacci Level Technical Analysis - KeyCorp

KEY: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 18, 2026 a 11:44 am

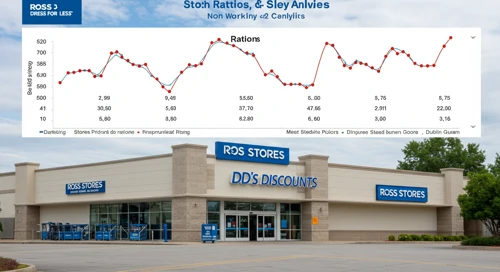

ROST: Fundamental Ratio Analysis - Ross Stores Inc

ROST: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 18, 2026 a 11:43 am

GEN: Fibunacci Level Technical Analysis - Gen Digital Inc

GEN: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 18, 2026 a 10:15 am

Industrial Comparison. 18 Jul

Comparison of Industrial. Where is strength and weakness? What has developed well and badly?

July 18, 2026 a 09:31 am

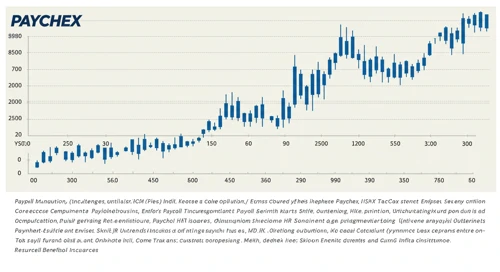

PAYX: Trend with Support and Resistance Levels - Paychex Inc

PAYX: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 18, 2026 a 09:03 am

Stock Market - Heatmap

Use mouse wheel to zoom in and out. Click a ticker to display detailed information in a new window. Hover mouse cursor over a ticker to see more data.

Stock's

RJF: Dividend Analysis - Raymond James Financial Inc

RJF: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 18, 2026 a 07:46 am

TROW: Fundamental Ratio Analysis - T Rowe Price Group Inc

TROW: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 18, 2026 a 07:43 am

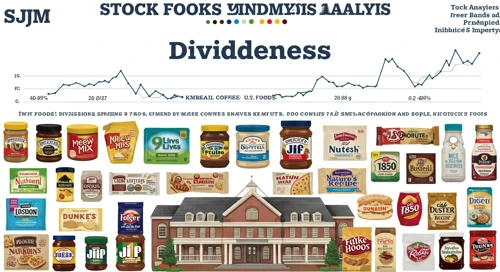

SJM: Dividend Analysis - The J M Smucker Company

SJM: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 18, 2026 a 07:31 am

AOS: Fibunacci Level Technical Analysis - A O Smith Corporation

AOS: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 18, 2026 a 06:44 am

JKHY: Fibunacci Level Technical Analysis - Jack Henry and Associates Inc

JKHY: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 18, 2026 a 05:15 am

CCL: Trend with Support and Resistance Levels - Carnival Corporation and plc

CCL: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 18, 2026 a 04:03 am

AXP: Dividend Analysis - American Express Company

AXP: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 18, 2026 a 03:31 am

ZBH: Analysts Ratings - Zimmer Biomet Holdings Inc

July 18, 2026 a 09:00 am

INTC: Analysts Ratings - Intel Corp

July 18, 2026 a 08:38 am

IFF: Trend with Support and Resistance Levels - International Flavors and Fragrances Inc

July 18, 2026 a 08:15 am

AVGO: Fundamental Ratio Analysis - Broadcom Inc

July 18, 2026 a 08:00 am

HOOD: Trend with Support and Resistance Levels - Robinhood Markets Inc

HOOD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 18, 2026 a 03:15 am

FDX: Dividend Analysis - FedEx Corporation

FDX: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 18, 2026 a 02:46 am

TRV: Analysts Ratings - The Travelers Companies Inc

TRV: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 17, 2026 a 09:00 pm

FI: Analysts Ratings - Fiserv Inc

FI: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 17, 2026 a 08:38 pm

ZBRA: Fundamental Ratio Analysis - Zebra Technologies Corporation

ZBRA: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 17, 2026 a 07:43 pm

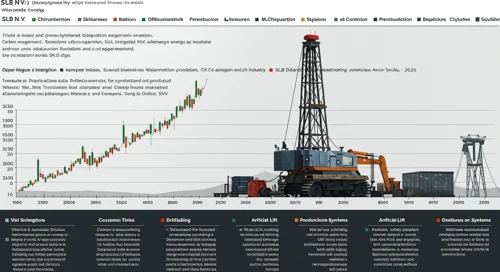

SLB: Fundamental Ratio Analysis - Slb NV

SLB: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 17, 2026 a 06:00 pm

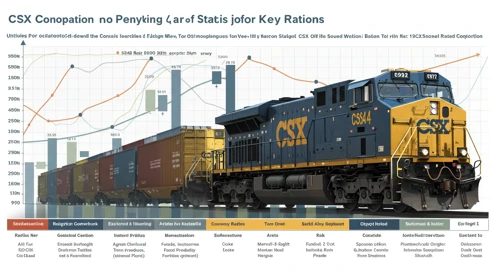

CSX: Analysts Ratings - CSX Corporation

CSX: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 17, 2026 a 05:00 pm

Economic Calendar

Currencies

GBPUSD: Fibunacci Level Technical Analysis

GBPUSD: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 17, 2026 a 05:08 am

CHFJPY: Trend with Support and Resistance Levels

CHFJPY: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 17, 2026 a 04:28 am

Todays Important Key Figures 16 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 16, 2026 a 07:00 pm

CADJPY: Fibunacci Level Technical Analysis

CADJPY: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 16, 2026 a 05:08 am

EURAUD: Trend with Support and Resistance Levels

EURAUD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 16, 2026 a 04:28 am

Important Key Figures of the last Days

Overview of key economic indicators released over the past days, highlighting their potential impact on markets and investor sentiment.

July 16, 2026 a 02:31 am

Todays Important Key Figures 15 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 15, 2026 a 07:00 pm

GBPCAD: Fibunacci Level Technical Analysis

July 18, 2026 a 05:08 am

NZDCAD: Trend with Support and Resistance Levels

July 18, 2026 a 04:28 am

Todays Important Key Figures 18 Jul

July 17, 2026 a 11:00 pm

Todays Important Key Figures 17 Jul

July 17, 2026 a 07:00 pm

CADCHF: Fibunacci Level Technical Analysis

CADCHF: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 15, 2026 a 05:08 am

GBPSEK: Trend with Support and Resistance Levels

GBPSEK: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 15, 2026 a 04:28 am

Todays Important Key Figures 14 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 14, 2026 a 07:00 pm

GBPCHF: Fibunacci Level Technical Analysis

GBPCHF: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 14, 2026 a 05:08 am

USDCHF: Trend with Support and Resistance Levels

USDCHF: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 14, 2026 a 04:28 am

Important Key Figures of the last Days

Overview of key economic indicators released over the past days, highlighting their potential impact on markets and investor sentiment.

July 14, 2026 a 02:31 am

Todays Important Key Figures 13 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 13, 2026 a 07:00 pm

Currencies