Todays Important Key Figures 09 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 09, 2026 a 07:00 pm

SCHW: Fundamental Ratio Analysis - The Charles Schwab Corporation

SCHW: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 09, 2026 a 06:01 pm

CI: Analysts Ratings - Cigna Corporation

CI: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 09, 2026 a 05:00 pm

FRT: Fibunacci Level Technical Analysis - Federal Realty Investment Trust

FRT: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 09, 2026 a 04:44 pm

PODD: Analysts Ratings - Insulet Corp

PODD: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 09, 2026 a 04:39 pm

EXC: Fundamental Ratio Analysis - Exelon Corporation

EXC: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 09, 2026 a 03:43 pm

PNR: Dividend Analysis - Pentair plc

PNR: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 09, 2026 a 03:31 pm

Todays Important Key Figures 10 Jul

July 09, 2026 a 11:01 pm

MCHP: Analysts Ratings - Microchip Technology Incorporated

July 09, 2026 a 09:00 pm

OTIS: Analysts Ratings - Otis Worldwide Corporation

July 09, 2026 a 08:38 pm

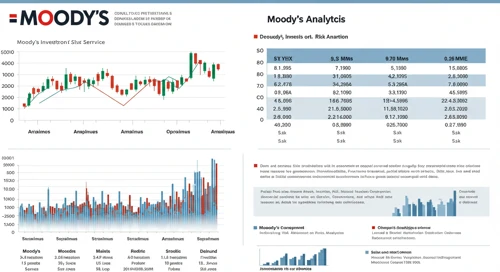

MCO: Fundamental Ratio Analysis - Moodys Corporation

July 09, 2026 a 07:43 pm

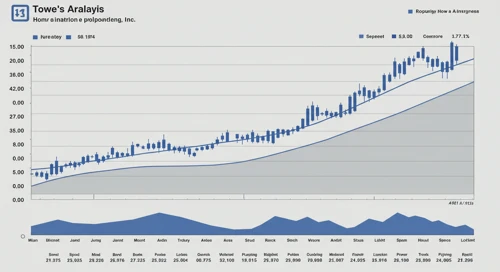

LOW: Fibunacci Level Technical Analysis - Lowes Companies Inc

LOW: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 09, 2026 a 03:15 pm

Financials Comparison. 09 Jul

Comparison of Financials. Where is strength and weakness? What has developed well and badly?

July 09, 2026 a 03:12 pm

PWR: Trend with Support and Resistance Levels - Quanta Services Inc

PWR: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 09, 2026 a 02:03 pm

AMAT: Trend with Support and Resistance Levels - Applied Materials Inc

AMAT: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 09, 2026 a 01:15 pm

VEEV: Fundamental Ratio Analysis - Veeva Systems Inc

VEEV: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 09, 2026 a 01:00 pm

PANW: Analysts Ratings - Palo Alto Networks Inc

PANW: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 09, 2026 a 01:00 pm

SW: Analysts Ratings - Smurfit Westrock plc

SW: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 09, 2026 a 12:38 pm

Stock Market - Heatmap

Use mouse wheel to zoom in and out. Click a ticker to display detailed information in a new window. Hover mouse cursor over a ticker to see more data.

Stock's

STT: Analysts Ratings - State Street Corporation

STT: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 09, 2026 a 09:00 am

HSY: Analysts Ratings - The Hershey Company

HSY: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 09, 2026 a 08:38 am

MLM: Trend with Support and Resistance Levels - Martin Marietta Materials Inc

MLM: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 09, 2026 a 08:15 am

FOXA: Fundamental Ratio Analysis - Fox Corporation

FOXA: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 09, 2026 a 08:00 am

DOV: Fundamental Ratio Analysis - Dover Corporation

DOV: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 09, 2026 a 07:43 am

HSY: Dividend Analysis - The Hershey Company

HSY: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 09, 2026 a 07:31 am

AEP: Fibunacci Level Technical Analysis - American Electric Power Company Inc

AEP: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 09, 2026 a 06:44 am

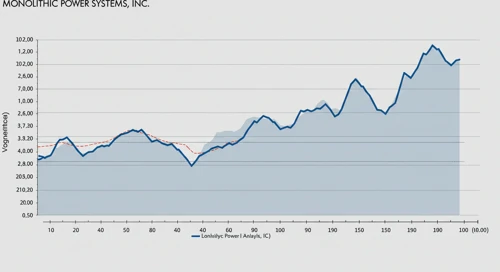

MPWR: Fibunacci Level Technical Analysis - Monolithic Power Systems Inc

July 09, 2026 a 11:44 am

APP: Fundamental Ratio Analysis - AppLovin Corporation

July 09, 2026 a 11:43 am

TKO: Dividend Analysis - TKO Group Holdings Inc

July 09, 2026 a 11:31 am

CASY: Fibunacci Level Technical Analysis - Caseys General Stores Inc

July 09, 2026 a 10:15 am

EXC: Fibunacci Level Technical Analysis - Exelon Corporation

EXC: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 09, 2026 a 05:15 am

BAC: Trend with Support and Resistance Levels - Bank of America Corporation

BAC: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 09, 2026 a 04:03 am

COR: Dividend Analysis - Cencora Inc

COR: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 09, 2026 a 03:30 am

FDXF: Trend with Support and Resistance Levels - FedEx Freight Holding Company Inc

FDXF: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 09, 2026 a 03:15 am

SBUX: Analysts Ratings - Starbucks Corporation

SBUX: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 08, 2026 a 09:00 pm

CRL: Analysts Ratings - Charles River Laboratories International Inc

CRL: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 08, 2026 a 08:38 pm

CI: Fundamental Ratio Analysis - Cigna Corporation

CI: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 08, 2026 a 07:43 pm

Economic Calendar

Currencies

USDCAD: Trend with Support and Resistance Levels

USDCAD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 08, 2026 a 04:28 am

Todays Important Key Figures 07 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 07, 2026 a 07:00 pm

GBPAUD: Fibunacci Level Technical Analysis

GBPAUD: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 07, 2026 a 05:08 am

NZDJPY: Trend with Support and Resistance Levels

NZDJPY: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 07, 2026 a 04:28 am

Important Key Figures of the last Days

Overview of key economic indicators released over the past days, highlighting their potential impact on markets and investor sentiment.

July 07, 2026 a 02:31 am

Todays Important Key Figures 06 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 06, 2026 a 07:00 pm

EURJPY: Fibunacci Level Technical Analysis

EURJPY: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 06, 2026 a 05:08 am

CADJPY: Fibunacci Level Technical Analysis

July 09, 2026 a 05:08 am

Important Key Figures of the last Days

July 09, 2026 a 02:31 am

Todays Important Key Figures 08 Jul

July 08, 2026 a 07:00 pm

AUDCAD: Fibunacci Level Technical Analysis

July 08, 2026 a 05:08 am

GBPCAD: Trend with Support and Resistance Levels

GBPCAD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 06, 2026 a 04:28 am

AUDJPY: Fibunacci Level Technical Analysis

AUDJPY: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 05, 2026 a 05:08 am

EURGBP: Trend with Support and Resistance Levels

EURGBP: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 05, 2026 a 04:28 am

GBPSEK: Fibunacci Level Technical Analysis

GBPSEK: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 04, 2026 a 05:08 am

USDCHF: Trend with Support and Resistance Levels

USDCHF: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 04, 2026 a 04:28 am

Todays Important Key Figures 04 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 03, 2026 a 11:00 pm

Todays Important Key Figures 03 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 03, 2026 a 07:00 pm

Currencies