HRL: Dividend Analysis - Hormel Foods Corporation

HRL: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 23, 2026 a 03:31 am

TPR: Trend with Support and Resistance Levels - Tapestry Inc

TPR: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 23, 2026 a 03:15 am

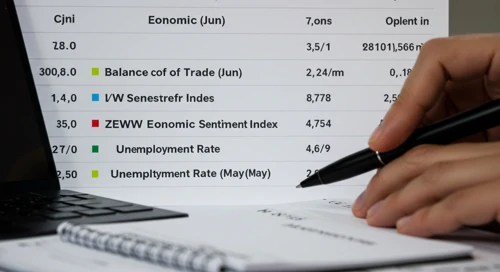

Important Key Figures of the last Days

Overview of key economic indicators released over the past days, highlighting their potential impact on markets and investor sentiment.

July 23, 2026 a 02:31 am

Todays Important Key Figures 23 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 22, 2026 a 11:00 pm

MTD: Analysts Ratings - Mettler Toledo International Inc

MTD: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 09:00 pm

ALGN: Analysts Ratings - Align Technology Inc

ALGN: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 08:38 pm

CMI: Fundamental Ratio Analysis - Cummins Inc

CMI: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 22, 2026 a 07:43 pm

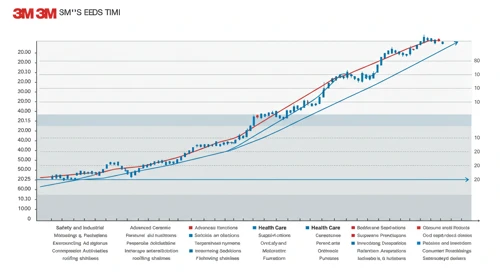

MMM: Fibunacci Level Technical Analysis - 3M Company

July 23, 2026 a 05:15 am

AUDNZD: Fibunacci Level Technical Analysis

July 23, 2026 a 05:08 am

CADCHF: Trend with Support and Resistance Levels

July 23, 2026 a 04:28 am

UDR: Trend with Support and Resistance Levels - UDR Inc

July 23, 2026 a 04:03 am

Todays Important Key Figures 22 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 22, 2026 a 07:00 pm

PH: Fundamental Ratio Analysis - Parker Hannifin Corporation

PH: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 22, 2026 a 06:00 pm

IEX: Analysts Ratings - IDEX Corporation

IEX: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 05:00 pm

PEP: Fibunacci Level Technical Analysis - PepsiCo Inc

PEP: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 22, 2026 a 04:44 pm

LNT: Analysts Ratings - Alliant Energy Corporation

LNT: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 04:38 pm

CHRW: Fundamental Ratio Analysis - CH Robinson Worldwide Inc

CHRW: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 22, 2026 a 03:43 pm

ICE: Dividend Analysis - Intercontinental Exchange Inc

ICE: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 22, 2026 a 03:31 pm

Stock Market - Heatmap

Use mouse wheel to zoom in and out. Click a ticker to display detailed information in a new window. Hover mouse cursor over a ticker to see more data.

Stock's

CARR: Analysts Ratings - Carrier Global Corporation

CARR: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 01:00 pm

MSFT: Dividend Analysis - Microsoft Corporation

MSFT: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 22, 2026 a 12:46 pm

LITE: Analysts Ratings - Lumentum Holdings Inc

LITE: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 12:38 pm

VLTO: Fibunacci Level Technical Analysis - Veralto Corporation

VLTO: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 22, 2026 a 11:44 am

VTRS: Fundamental Ratio Analysis - Viatris Inc

VTRS: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 22, 2026 a 11:43 am

FIX: Dividend Analysis - Comfort Systems USA Inc

FIX: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 22, 2026 a 11:31 am

WYNN: Fibunacci Level Technical Analysis - Wynn Resorts Limited

WYNN: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 22, 2026 a 10:15 am

ERIE: Fibunacci Level Technical Analysis - Erie Indemnity Company

July 22, 2026 a 03:15 pm

KVUE: Trend with Support and Resistance Levels - Kenvue Inc

July 22, 2026 a 02:03 pm

AME: Trend with Support and Resistance Levels - AMETEK Inc

July 22, 2026 a 01:15 pm

WMT: Fundamental Ratio Analysis - Walmart Inc

July 22, 2026 a 01:00 pm

MSFT: Trend with Support and Resistance Levels - Microsoft Corporation

MSFT: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 22, 2026 a 09:03 am

TJX: Analysts Ratings - The TJX Companies Inc

TJX: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 09:00 am

ULTA: Analysts Ratings - Ulta Beauty Inc

ULTA: Comprehensive breakdown of current and historical analyst ratings, offering insights into how expert sentiment has evolved over time.

July 22, 2026 a 08:38 am

ATO: Trend with Support and Resistance Levels - Atmos Energy Corporation

ATO: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 22, 2026 a 08:15 am

WDC: Fundamental Ratio Analysis - Western Digital Corporation

WDC: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 22, 2026 a 08:00 am

BLK: Dividend Analysis - BlackRock Inc

BLK: In-depth analysis of a company's dividend stability and key fundamental ratios to assess its financial strength and long-term investment potential.

July 22, 2026 a 07:46 am

AIG: Fundamental Ratio Analysis - American International Group Inc

AIG: Evaluation of key financial ratios, analyst ratings, and price targets. A data-driven perspective on the valuation and market expectations.

July 22, 2026 a 07:43 am

Economic Calendar

Currencies

AUDUSD: Trend with Support and Resistance Levels

AUDUSD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 21, 2026 a 04:28 am

Important Key Figures of the last Days

Overview of key economic indicators released over the past days, highlighting their potential impact on markets and investor sentiment.

July 21, 2026 a 02:31 am

Todays Important Key Figures 20 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 20, 2026 a 07:00 pm

EURCHF: Fibunacci Level Technical Analysis

EURCHF: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 20, 2026 a 05:08 am

EURUSD: Trend with Support and Resistance Levels

EURUSD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 20, 2026 a 04:28 am

GBPAUD: Fibunacci Level Technical Analysis

GBPAUD: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 19, 2026 a 05:08 am

GBPNZD: Trend with Support and Resistance Levels

GBPNZD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 19, 2026 a 04:28 am

GBPSEK: Fibunacci Level Technical Analysis

July 22, 2026 a 05:08 am

EURJPY: Trend with Support and Resistance Levels

July 22, 2026 a 04:28 am

Todays Important Key Figures 21 Jul

July 21, 2026 a 07:00 pm

GBPJPY: Fibunacci Level Technical Analysis

July 21, 2026 a 05:08 am

GBPCAD: Fibunacci Level Technical Analysis

GBPCAD: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 18, 2026 a 05:08 am

NZDCAD: Trend with Support and Resistance Levels

NZDCAD: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 18, 2026 a 04:28 am

Todays Important Key Figures 18 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 17, 2026 a 11:00 pm

Todays Important Key Figures 17 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 17, 2026 a 07:00 pm

GBPUSD: Fibunacci Level Technical Analysis

GBPUSD: Fibonacci retracement levels to identify key potential support and resistance zones, based on recent price trends.

July 17, 2026 a 05:08 am

CHFJPY: Trend with Support and Resistance Levels

CHFJPY: Current price trend is evaluated alongside key support and resistance level. View of potential turning points and price momentum.

July 17, 2026 a 04:28 am

Todays Important Key Figures 16 Jul

Today’s important economic data releases – a snapshot of key indicators influencing markets and shaping financial expectations.

July 16, 2026 a 07:00 pm

Currencies