April 06, 2026 a 06:00 pm

MOS: Fundamental Ratio Analysis - The Mosaic Company

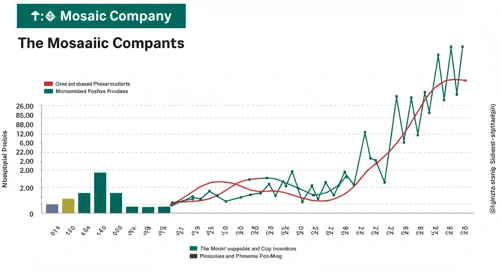

The Mosaic Company (MOS) stands strong in agricultural inputs, focusing on phosphate and potash crop nutrients. The company has demonstrated consistent performance in its financial metrics, reflecting a stable position in its sector. However, its debt ratios highlight potential financial leverage concerns.

Fundamental Rating

The fundamental ratings of Mosaic indicate a solid performance, with room for improvement in leveraging and valuation metrics.

| Category | Score | Visualization |

|---|---|---|

| Discounted Cash Flow | 4 | |

| Return on Equity | 4 | |

| Return on Assets | 5 | |

| Debt to Equity | 1 | |

| Price to Earnings | 3 | |

| Price to Book | 4 |

Historical Rating

Comparing historical data shows consistency in most areas, though changes over time should be monitored for informed decision-making.

| Date | Overall | DCF | ROE | ROA | Debt/Equity | P/E | P/B |

|---|---|---|---|---|---|---|---|

| 2026-04-06 | 4 | 4 | 4 | 5 | 1 | 3 | 4 |

| Previous | 0 | 4 | 4 | 5 | 1 | 3 | 4 |

Analyst Price Targets

Analysts project modest growth opportunities with reserved estimates on the stock's price target.

| High | Low | Median | Consensus |

|---|---|---|---|

| $44 | $27 | $33.5 | $33.8 |

Analyst Sentiment

The sentiment around MOS is predominantly neutral, with a higher number of hold ratings than buy or sell recommendations.

| Rating | Count | Visualization |

|---|---|---|

| Strong Buy | 0 | |

| Buy | 14 | |

| Hold | 28 | |

| Sell | 7 | |

| Strong Sell | 0 |

Conclusion

The Mosaic Company is well-positioned within the agricultural inputs industry, with a strong focus on essential crop nutrients. Despite a solid fundamental rating, its debt-to-equity ratio may warrant investor caution. Analyst sentiment reflects a cautious outlook, which may impact short-term gains. However, long-term growth potential remains viable given current market dynamics. Investors should weigh these factors carefully before deciding.

Smart Data Insight

Master the Perfect Entry & Exit for this Stock

Don't leave your profits to chance. Historically, this stock follows specific seasonal patterns that institutional traders use to maximize returns.

- ✅ Identify the "Golden Buying Window"

- ✅ Avoid high-risk correction cycles

- ✅ Backtested data from the last 20+ years