February 19, 2026 a 07:31 am

MAR: Dividend Analysis - Marriott International, Inc.

The Marriott International, Inc. presents a solid dividend profile characterized by a modest yield and stable historical payouts. With a dividend history spanning 28 years and a commitment to growth, it stands out in the hospitality sector. The company's financial metrics exhibit prudent payout ratios, suggesting room for further dividend enhancements.

Overview 📊

Marriott International operates within the hospitality sector, offering a current dividend yield of 0.75%. At 2.67 USD per share, the dividend has been consistent for 28 years without any recent cuts. This reflects the company's financial resilience and commitment to shareholder returns.

| Description | Detail |

|---|---|

| Sector | Hospitality |

| Dividend yield | 0.75 % |

| Current dividend per share | 2.67 USD |

| Dividend history | 28 years |

| Last cut or suspension | None |

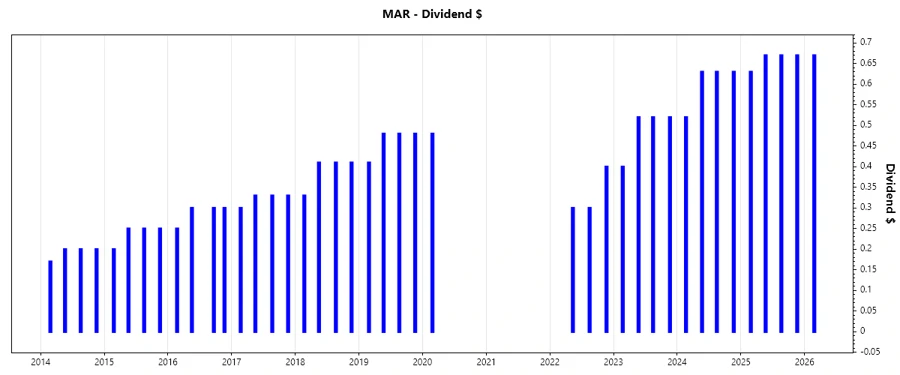

Dividend History 🗣️

Marriott's commitment to its dividend policy is evident from its 28-year history without any interruptions. This stability is reassuring for investors looking for reliable income.

| Year | Dividend Per Share (USD) |

|---|---|

| 2026 | 0.67 |

| 2025 | 2.64 |

| 2024 | 2.41 |

| 2023 | 1.96 |

| 2022 | 1.0 |

Dividend Growth 📈

The growth trajectory for Marriott's dividends over both 3 and 5 years indicates a strategy of moderate yet steady increases, supporting sustained shareholder value enhancement.

| Time | Growth |

|---|---|

| 3 years | 38.21 % |

| 5 years | 40.63 % |

The average dividend growth is 40.63 % over 5 years. This shows moderate but steady dividend growth.

Payout Ratio ✅

Payout ratios are critical for assessing the sustainability of dividends. Marriott's current ratios suggest ample coverage, ensuring dividends are well-supported by earnings and cash flows.

| Key figure | Ratio |

|---|---|

| EPS-based | 27.6 % |

| Free cash flow-based | 24.45 % |

With a payout ratio of 27.6 % (EPS) and 24.45 % (FCF), Marriott maintains a conservative approach, indicating robust dividend security.

Cashflow & Capital Efficiency

Cash flow and capital efficiency metrics are fundamental in evaluating Marriott's financial health and its ability to fund dividends through operations.

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Free Cash Flow Yield | 3.98 % | 2.52 % | 3.86 % |

| Earnings Yield | 4.53 % | 3.00 % | 3.12 % |

| CAPEX to Operating Cash Flow | 14.26 % | 27.28 % | 18.80 % |

| Stock-based Compensation to Revenue | 0.86 % | 0.94 % | 0.90 % |

| Free Cash Flow / Operating Cash Flow Ratio | 85.74 % | 72.72 % | 100 % |

Marriott exhibits strong cash flow management, crucial for sustaining its growth and investment aspirations.

Balance Sheet & Leverage Analysis

The balance sheet indicators reveal Marriott's leverage strategies and potential financial flexibility, crucial in market volatility.

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Debt-to-Equity | -18.71 | -5.09 | -4.53 |

| Debt-to-Assets | 49.70 % | 58.21 % | 62.03 % |

| Debt-to-Capital | 105.65 % | 124.43 % | 128.33 % |

| Net Debt to EBITDA | 2.84 | 3.42 | 3.73 |

| Current Ratio | 0.43 | 0.40 | 0.43 |

| Quick Ratio | 0.43 | 0.40 | 0.43 |

| Financial Leverage | -37.65 | -8.75 | -7.30 |

Marriott's leverage ratios are notably high, indicating potential room for balance sheet improvement and risk mitigation.

Fundamental Strength & Profitability

The fundamental strength and profitability metrics underscore Marriott's operational efficiencies and return metrics for assessing long-term investment potential.

| Year | 2023 | 2024 | 2025 |

|---|---|---|---|

| Return on Equity | -452.05 % | -79.38 % | -68.97 % |

| Return on Assets | 12.01 % | 9.07 % | 9.44 % |

| Margins: Net | 13.00 % | 9.46 % | 9.93 % |

| EBIT Margin | 16.63 % | 15.32 % | 16.00 % |

| EBITDA Margin | 18.47 % | 17.28 % | 17.14 % |

| Gross Margin | 21.61 % | 20.32 % | 21.34 % |

| R&D to Revenue | 0 % | 0 % | 0 % |

Despite certain challenges, Marriott showcases solid margins and asset utilization, crucial for steady profitability amidst market fluctuations.

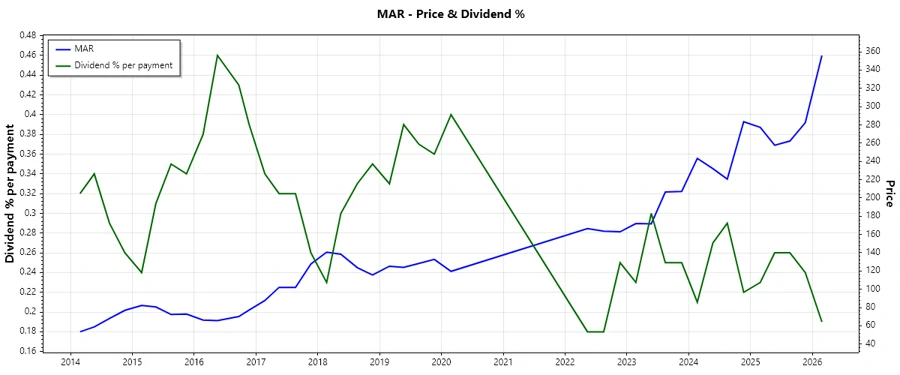

Price Development 📉

Dividend Scoring System ✅

| Category | Score | Score Bar |

|---|---|---|

| Dividend yield | 3 | |

| Dividend Stability | 5 | |

| Dividend growth | 4 | |

| Payout ratio | 5 | |

| Financial stability | 3 | |

| Dividend continuity | 5 | |

| Cashflow Coverage | 4 | |

| Balance Sheet Quality | 2 |

Total Score: 31/40

Rating 🗣️

Marriott International, Inc. maintains a robust dividend policy, offering reliability through stable payouts and consistent growth. Despite certain leverage concerns, its healthy cash flow and earnings yield ensure continued dividend security. As such, the stock is recommended for income-focused portfolios with a long-term investment horizon.

Smart Data Insight

Master the Perfect Entry & Exit for this Stock

Don't leave your profits to chance. Historically, this stock follows specific seasonal patterns that institutional traders use to maximize returns.

- ✅ Identify the "Golden Buying Window"

- ✅ Avoid high-risk correction cycles

- ✅ Backtested data from the last 20+ years