November 20, 2025 a 07:46 am

JBHT: Dividend Analysis - J.B. Hunt Transport Services, Inc.

J.B. Hunt Transport Services, Inc. presents a stable dividend profile with a moderate yield of 1.03%. Its long history of dividend payments spanning 38 years reflects resilience and consistency. As the company continues to navigate market dynamics, investors may find the steady dividend policy reassuring, although the yield may not be particularly high compared to other sectors.

📊 Overview

The overview of J.B. Hunt Transport Services, Inc.'s dividend profile provides key insights into its sector performance and dividend metrics:

| Metric | Value |

|---|---|

| Sector | Transportation |

| Dividend yield | 1.03% |

| Current dividend per share | 1.72 USD |

| Dividend history | 38 years |

| Last cut or suspension | 2013 |

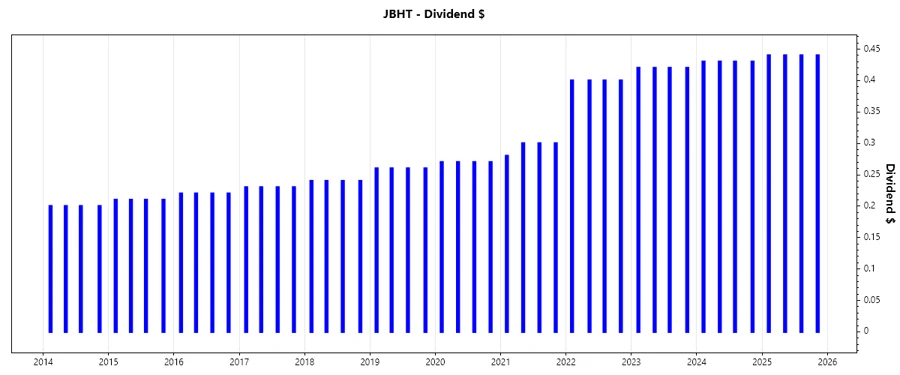

📈 Dividend History

The dividend history of a company is crucial as it indicates reliability and trustworthiness in returning value to shareholders over time.

| Year | Dividend per Share (USD) |

|---|---|

| 2025 | 1.76 |

| 2024 | 1.72 |

| 2023 | 1.68 |

| 2022 | 1.60 |

| 2021 | 1.18 |

📊 Dividend Growth

Dividend growth is a strong indicator of a company's ability to increase dividend payouts over time, reflecting its growth potential and financial strength.

| Time | Growth |

|---|---|

| 3 years | 13.38% |

| 5 years | 10.59% |

The average dividend growth is 10.59% over 5 years. This shows moderate but steady dividend growth.

✅ Payout Ratio

The payout ratio indicates how much of a company's earnings and free cash flow are distributed as dividends to shareholders. It can reflect the sustainability of dividend payments.

| Key Figure | Ratio |

|---|---|

| EPS-based | 29.59% |

| Free cash flow-based | 20.77% |

The EPS payout ratio of 29.59% and the FCF payout ratio of 20.77% indicate a conservative approach to dividend distribution, suggesting dividends are well-covered by earnings and cash flow.

📊 Cashflow & Capital Efficiency

An analysis of cash flows alongside capital efficiency metrics helps assess the operational efficiency and financial health of J.B. Hunt Transport Services, Inc.

| Year | 2023 | 2022 |

|---|---|---|

| Free Cash Flow Yield | -0.57% | 1.30% |

| Earnings Yield | 3.53% | 5.34% |

| CAPEX/Ope. Cash Flow | 106.75% | 86.71% |

| Stock-based Comp./Revenue | 0.62% | 0.52% |

| Free Cash Flow/Ope. Cash Flow | -6.75% | 13.29% |

The data suggest free cash flow challenges in recent periods, although earnings yield remains positive. Capital expenditures have outstripped operating cash flow, raising concerns about capital efficiency.

📊 Balance Sheet & Leverage Analysis

Understanding leverage ratios and balance sheet strength is crucial for gauging financial stability and risk profile.

| Year | 2023 | 2022 |

|---|---|---|

| Debt-to-Equity | 47.00% | 42.85% |

| Debt-to-Assets | 21.91% | 19.63% |

| Debt-to-Capital | 31.97% | 29.99% |

| Net Debt to EBITDA | 1.08 | 0.77 |

| Current Ratio | 1.35 | 1.41 |

| Quick Ratio | 1.32 | 1.38 |

| Financial Leverage | 2.15 | 2.18 |

J.B. Hunt's debt levels are manageable with leverage ratios reflecting a balanced approach to debt usage. The company's current and quick ratios indicate adequate liquidity.

📊 Fundamental Strength & Profitability

Examining profitability and efficiency metrics provides insight into the company's operational and financial prowess.

| Year | 2023 | 2022 |

|---|---|---|

| Return on Equity | 17.75% | 26.44% |

| Return on Assets | 8.27% | 12.11% |

| Net Profit Margin | 5.68% | 6.54% |

| EBIT Margin | 7.80% | 8.99% |

| EBITDA Margin | 13.55% | 13.35% |

| Gross Margin | 17.23% | 16.69% |

| R&D to Revenue | 0% | 0% |

Strong returns on equity and assets suggest effective management and profitable operations. Despite no spending on R&D, the profitability margins confirm the company's financial health.

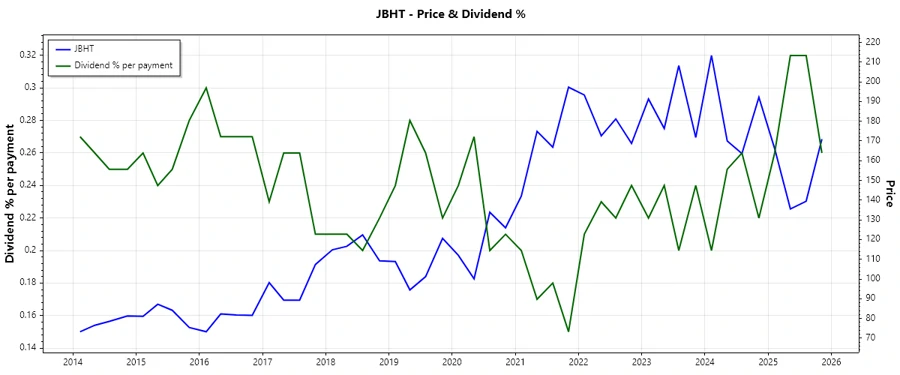

📈 Price Development

🗣️ Dividend Scoring System

| Category | Score | |

|---|---|---|

| Dividend yield | 2 | |

| Dividend Stability | 5 | |

| Dividend growth | 3 | |

| Payout ratio | 4 | |

| Financial stability | 4 | |

| Dividend continuity | 5 | |

| Cashflow Coverage | 3 | |

| Balance Sheet Quality | 4 |

Total Score: 30/40

✅ Rating

J.B. Hunt Transport Services, Inc. earns a strong overall rating due to its consistency in dividend payments and robust financial health. While the yield may seem modest, the stability and growth make it a reliable choice for investors seeking a blend of income and growth. Investors should consider this stock if they value long-term dividend reliability over high immediate yield.

Smart Data Insight

Master the Perfect Entry & Exit for this Stock

Don't leave your profits to chance. Historically, this stock follows specific seasonal patterns that institutional traders use to maximize returns.

- ✅ Identify the "Golden Buying Window"

- ✅ Avoid high-risk correction cycles

- ✅ Backtested data from the last 20+ years