May 30, 2025 a 08:38 am

INVH: Analysts Ratings - Invitation Homes Inc.

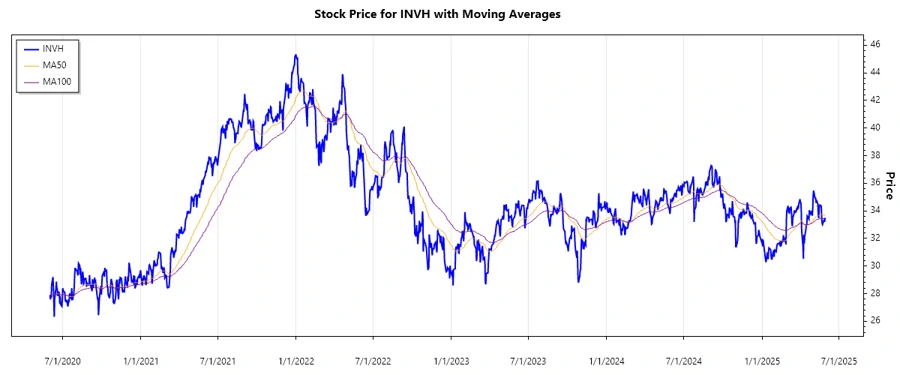

Invitation Homes Inc. has consistently demonstrated a robust ability to adapt and meet the evolving demands of the residential real estate market. As the leading single-family home leasing company in the United States, its focus on high-quality homes situated near essential amenities such as jobs and schools positions it well to cater to modern lifestyle demands. Continual high-touch service and resident experience enhancement are key operational strategies that bolster its market appeal and investor confidence.

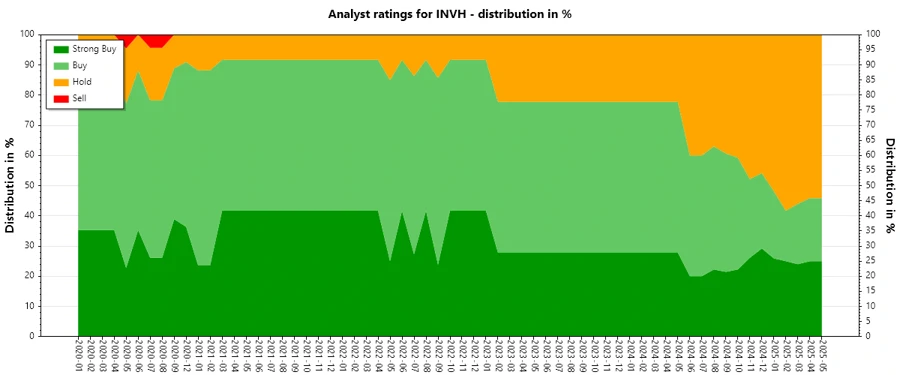

Historical Stock Grades

| Rating | Count | Score |

|---|---|---|

| Strong Buy | 6 | |

| Buy | 5 | |

| Hold | 13 | |

| Sell | 0 | |

| Strong Sell | 0 |

Sentiment Development

The invitation Homes Inc. analysis reveals a noticeable trend towards more conservative recommendations, with an increase in 'Hold' ratings over the months. This suggests a cautious approach from analysts, with the current market environment possibly influencing their decisions.

- Stable 'Strong Buy' ratings with slight fluctuations observed.

- Consistent 'Buy' recommendations, suggesting a maintained investor confidence.

- A significant rise in 'Hold' ratings in recent months.

Percentage Trends

The percentage breakdown of analyst ratings shows a steady shift towards more equilibrium in investor sentiment. A prominent rise in 'Hold' recommendations indicates a potential cautious outlook. This shift may reflect considerations of macroeconomic factors impacting the residential leasing sector.

- Strong Buy represents 20% – consistent over several months.

- Buy recommendations have seen a slight decrease to 16.67%.

- Hold now constitutes the majority at 43.33%.

Latest Analyst Recommendations

The latest analyst recommendations indicate stability and a consensus on the current rating stance. The maintenance of existing ratings underscores a confidence in the long-term outlook despite current uncertainties.

| Date | New Recommendation | Last Recommendation | Publisher |

|---|---|---|---|

| 2025-05-12 | Sector Perform | Sector Perform | Scotiabank |

| 2025-05-09 | Overweight | Overweight | Barclays |

| 2025-05-09 | Outperform | Outperform | Raymond James |

| 2025-05-06 | Outperform | Outperform | Oppenheimer |

| 2025-05-06 | Buy | Buy | Goldman Sachs |

Analyst Recommendations with Change of Opinion

Recent changes in analyst recommendations reveal notable upgrades and downgrades that could indicate shifts in market sentiment. Such changes may reflect adjustments in macroeconomic outlooks or company-specific developments.

| Date | New Recommendation | Last Recommendation | Publisher |

|---|---|---|---|

| 2025-03-13 | Outperform | Neutral | Mizuho |

| 2025-01-24 | Equal Weight | Overweight | Morgan Stanley |

| 2025-01-21 | Hold | Buy | Deutsche Bank |

| 2024-09-24 | Neutral | Buy | B of A Securities |

| 2024-09-09 | Sector Perform | Outperform | RBC Capital |

Interpretation

Overall, the growing number of 'Hold' ratings in the analyst community signals a more cautious market sentiment towards Invitation Homes Inc. While consistent positive recommendations such as 'Buy' and 'Strong Buy' persist, they seem increasingly tempered by an increase in neutral positions. This balance suggests a recognition of the company's strengths amidst broader market uncertainties.

Conclusion

In summary, Invitation Homes Inc. continues to hold a solid position in its domain, with analysts showing a balanced view between growth potential and market challenges. The consistent trend of 'Hold' recommendations suggests careful optimism, supported by stable 'Buy' ratings. Investors should weigh current market dynamics against Invitation Homes' strategic advantages as they consider future engagements.