May 29, 2026 a 07:31 am

EMR: Dividend Analysis - Emerson Electric Co.

Emerson Electric Co. (EMR) has demonstrated a resilient dividend history with over 55 years of continuous payouts, a testament to its robust business model. The company maintains a disciplined payout policy, with a current reasonable dividend yield of 1.65%. While the growth in dividends has been modest, it underscores stability, appealing to investors seeking reliable income. Additionally, Emerson's prudent payout ratios ensure that dividends are well-covered by both earnings and free cash flow, indicating a sustainable distribution capacity.

📊 Overview

Emerson Electric Co. operates within the Industrial Goods sector, offering a dividend yield that, while not the highest in the market, exemplifies consistency and dependability. Investors should appreciate the company's strong 55-year history of dividend distributions, uninterrupted by cuts or suspensions, suggesting a commitment to shareholder value.

| Category | Value |

|---|---|

| Sector | Industrial Goods |

| Dividend yield | 1.65 % |

| Current dividend per share | 2.12 USD |

| Dividend history | 55 years |

| Last cut or suspension | None |

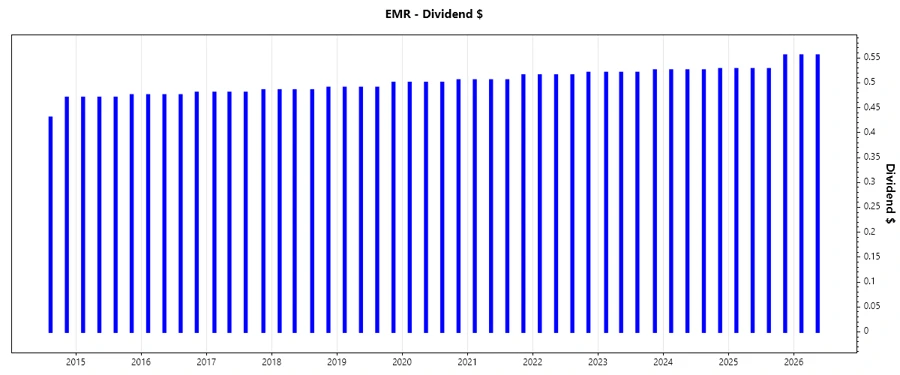

🗣️ Dividend History

The longevity of Emerson's dividend payment is noteworthy, highlighting a reliable and consistent income source for investors who value stable cash inflows. Such a history suggests resilience through various economic cycles and a strong emphasis on returning capital to shareholders.

| Year | Dividend per Share (USD) |

|---|---|

| 2026 | 1.110 |

| 2025 | 2.1375 |

| 2024 | 2.1025 |

| 2023 | 2.085 |

| 2022 | 2.065 |

📈 Dividend Growth

Emerson's dividend growth has been steady yet conservative over the past few years, indicative of a cautious approach to capital allocation. This strategy is particularly appealing to investors seeking gradual but reliable growth in income.

| Time | Growth |

|---|---|

| 3 years | 1.16 % |

| 5 years | 1.29 % |

The average dividend growth is 1.29 % over 5 years. This shows moderate but steady dividend growth.

⚠️ Payout Ratio

The payout ratio is a critical measure of dividend sustainability, reflecting the proportion of earnings a company returns to shareholders. Emerson's ratios suggest prudent financial management, maintaining a balance between returning capital and supporting business growth.

| Key figure | Ratio |

|---|---|

| EPS-based | 48.58 % |

| Free cash flow-based | 38.08 % |

Emerson's payout ratios indicate a conservative yet effective use of earnings and cash flow to fund its dividends, with 48.58 % from EPS and 38.08 % from FCF, showcasing a strong dividend cover.

📊 Cashflow & Capital Efficiency

Analyzing cash flow metrics provides insights into a company's ability to sustain operations and pay dividends. Emerson's cash flow efficiency indicates solid capital management, vital for maintaining dividend payments and long-term business health.

| Metrics | 2023 | 2024 | 2025 |

|---|---|---|---|

| Free Cash Flow Yield | 0.49 % | 4.66 % | 3.61 % |

| Earnings Yield | 23.84 % | 3.15 % | 3.11 % |

| CAPEX to Operating Cash Flow | 56.99 % | 12.58 % | 13.91 % |

| Stock-based Compensation to Revenue | 1.65 % | 1.49 % | 1.46 % |

| Free Cash Flow / Operating Cash Flow Ratio | 43.01 % | 87.42 % | 86.09 % |

Emerson's cash flow stability and capital utilization reflect efficient operational management, essential for regular dividend payouts and future growth investments.

📊 Balance Sheet & Leverage Analysis

A company's balance sheet health is paramount in assessing its ability to sustain dividends and navigate financial challenges. Emerson's leverage ratios exhibit manageable debt levels and robust liquidity, ensuring financial stability.

| Metrics | 2023 | 2024 | 2025 |

|---|---|---|---|

| Debt-to-Equity | 0.41 | 0.39 | 0.68 |

| Debt-to-Assets | 0.20 | 0.19 | 0.33 |

| Debt-to-Capital | 0.29 | 0.28 | 0.40 |

| Net Debt to EBITDA | 0.12 | 1.18 | 2.52 |

| Current Ratio | 2.75 | 1.77 | 0.87 |

| Quick Ratio | 2.35 | 1.39 | 0.65 |

| Financial Leverage | 2.07 | 2.05 | 2.07 |

The financial metrics reflect a strategically managed leverage position, supporting fiscal discipline and dividend issuance capability.

📊 Fundamental Strength & Profitability

Emerson's fundamental strength underscores its competitive positioning and ability to generate returns efficiently. The return metrics and margin performance affirm operational efficiency and profitability.

| Metrics | 2023 | 2024 | 2025 |

|---|---|---|---|

| Return on Equity | 63.89 % | 9.10 % | 11.31 % |

| Return on Assets | 30.92 % | 4.45 % | 5.46 % |

| Net Profit Margin | 87.17 % | 11.25 % | 12.73 % |

| EBIT Margin | 20.86 % | 13.39 % | 18.43 % |

| EBITDA Margin | 27.79 % | 23.05 % | 26.86 % |

| Gross Margin | 48.97 % | 50.79 % | 52.84 % |

The strong return metrics and stable margins illustrate Emerson's capacity to maintain profitability in diverse market conditions.

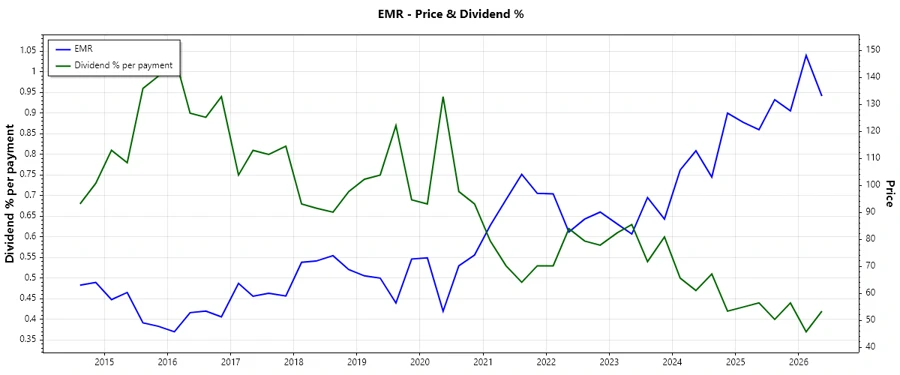

📊 Price Development

📊 Dividend Scoring System

| Criterion | Score (out of 5) | |

|---|---|---|

| Dividend yield | 3 | |

| Dividend Stability | 5 | |

| Dividend growth | 3 | |

| Payout ratio | 4 | |

| Financial stability | 4 | |

| Dividend continuity | 5 | |

| Cashflow Coverage | 4 | |

| Balance Sheet Quality | 4 |

Total Score: 32/40

✅ Rating

Emerson Electric Co.'s dividend profile is robust, marked by a commendable history of payouts and a solid financial foundation, making it a reliable choice for income-focused investors. While growth has been modest, the company's financial prudence and operational stability offer a reassuring long-term investment prospect. Recommend cautious optimism with an emphasis on reinvestment potentials within a diversified portfolio strategy.

Smart Data Insight

Master the Perfect Entry & Exit for this Stock

Don't leave your profits to chance. Historically, this stock follows specific seasonal patterns that institutional traders use to maximize returns.

- ✅ Identify the "Golden Buying Window"

- ✅ Avoid high-risk correction cycles

- ✅ Backtested data from the last 20+ years