December 24, 2025 a 07:46 am

📊 Dividend Analysis - Dominion Energy, Inc.

Dominion Energy, Inc. presents a mixed dividend profile with a high dividend yield of 4.57% and a long history of 42 years of dividend payments. However, recent years have shown challenges, particularly with a last dividend cut in 2021. Careful consideration of these dynamics is crucial for potential investors.

🔍 Overview

The overview assesses key dividend metrics that frame the financial landscape of Dominion Energy, Inc. Despite a long-standing tradition of dividends, the recent payout ratios pose red flags.

| Key Metric | Value |

|---|---|

| Sector | Utilities |

| Dividend Yield | 4.57 % |

| Current Dividend per Share | 2.67 USD |

| Dividend History | 42 years |

| Last Cut or Suspension | 2021 |

📉 Dividend History

The consistency of Dominion Energy’s dividend payments highlights stable cash-generating capability. However, the stability was disrupted in 2021, a crucial year indicating management's strategies under financial constraints.

| Year | Dividend per Share (USD) |

|---|---|

| 2025 | 2.67 |

| 2024 | 2.67 |

| 2023 | 2.67 |

| 2022 | 2.67 |

| 2021 | 2.52 |

📈 Dividend Growth

The growth dynamics present a complex picture. While there is slight recent growth, the longer-term decline may concern potential investors who prioritize growth.

| Time | Growth |

|---|---|

| 3 Years | 1.95 % |

| 5 Years | -6.16 % |

The average dividend growth is -6.16 % over 5 years. This shows a need for investors to remain cautious of long-term growth potential.

💡 Payout Ratio

The payout ratio is a critical financial metric that assesses the sustainability of dividends by comparing dividends per share to earnings. A high or negative payout ratio may indicate potential difficulty in maintaining current dividend levels.

| Key figure | Ratio |

|---|---|

| EPS-based | 97.32 % |

| Free Cash Flow-based | -148.81 % |

The payout ratios raise concern, particularly the FCF-based payout ratio, which indicates outflows exceeding inflows—potentially unsustainable over the long term.

📊 Cashflow & Capital Efficiency

Cash flow and capital efficiency are critical as they directly impact a company's ability to cover dividend payments. Analysis of recent financial figs suggests potential issues.

| Year | 2024 | 2023 | 2022 |

|---|---|---|---|

| Free Cash Flow Yield | -16.39% | -9.69% | -8.03% |

| Earnings Yield | 4.70% | 5.28% | 2.61% |

| CAPEX to Operating Cash Flow | 247.65% | 155.74% | 209.68% |

| Stock-based Compensation to Revenue | 0% | 0% | 0% |

| Free Cash Flow / Operating Cash Flow Ratio | -147.65% | -55.73% | -109.68% |

The figures present a challenging scenario for Dominion Energy's cash flow and capital efficiency, marked by negative cash flow yield and high CAPEX to operating cash flow.

🏦 Balance Sheet & Leverage Analysis

This analysis focuses on the financial stability and leverage of the company, impacting strategic decisions and dividend security.

| Year | 2024 | 2023 | 2022 |

|---|---|---|---|

| Debt-to-Equity | 1.53 | 1.61 | 1.49 |

| Debt-to-Assets | 0.41 | 0.41 | 0.39 |

| Debt-to-Capital | 0.61 | 0.62 | 0.60 |

| Net Debt to EBITDA | 6.18 | 6.46 | 6.45 |

| Current Ratio | 0.71 | 1.04 | 0.73 |

While the balancing sheet ratios suggest significant leverage, careful analysis of the coverage abilities is essential, taking leverage ratios into particular account.

📈 Fundamental Strength & Profitability

This section analyzes fundamental profitability and return measures critical for shareholders assessing growth potential and financial health.

| Year | 2024 | 2023 | 2022 |

|---|---|---|---|

| Return on Equity | 7.79% | 7.24% | 4.78% |

| Return on Assets | 2.07% | 1.83% | 1.26% |

| Margins: Net, EBIT, EBITDA, Gross | 14.69%, 28.14%, 46.39%, 47.87% | 13.85%, 25.67%, 47.40%, 48.34% | 9.48%, 23.39%, 45.72%, 45.75% |

| Research & Development to Revenue | 0% | 0% | 0% |

The fundamentals are varied with strong margins, yet high leverage and poor asset returns decreasing overall attractiveness as an investment.

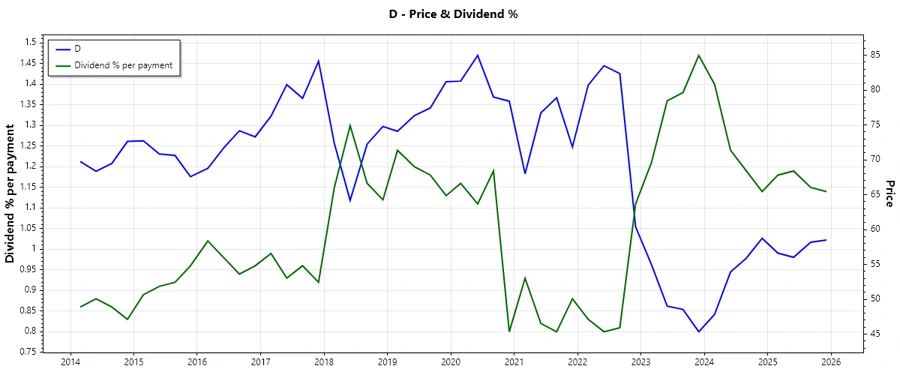

📉 Price Development

✅ Dividend Scoring System

| Category | Score (1-5) | Score Bar |

|---|---|---|

| Dividend yield | 4 | |

| Dividend Stability | 3 | |

| Dividend growth | 2 | |

| Payout ratio | 2 | |

| Financial stability | 3 | |

| Dividend continuity | 4 | |

| Cashflow Coverage | 2 | |

| Balance Sheet Quality | 3 |

Total Score: 23/40

🏆 Rating

Dominion Energy, Inc. posits a mixed dividend outlook, with notable strengths in yield and continuity but overshadowed by weak growth and potential payout sustainability issues. It’s a cautious 'Hold' for portfolios, considering potential improvements in cash flow and balance stability.