December 28, 2025 a 02:47 am

CL: Dividend Analysis - Colgate-Palmolive Company

Colgate-Palmolive Company exhibits a remarkable track record in dividend distributions, boasting over five decades of consistent increases, though its recent payout ratio and modest growth rates call for scrutiny. An imperative analysis reveals a solid yield with a challenge in growth acceleration.

📊 Overview

Colgate-Palmolive operates within the Consumer Goods sector, contributing to the appeal of its dividend profile. It maintains a steady dividend yield of 2.61%, paired with a recent dividend per share of 2.19 USD. The company's 54-year history of dividend payouts remains a testament to its stability.

| Category | Detail |

|---|---|

| Sector | Consumer Goods |

| Dividend yield | 2.61% |

| Current dividend per share | 2.19 USD |

| Dividend history | 54 years |

| Last cut or suspension | 2026 |

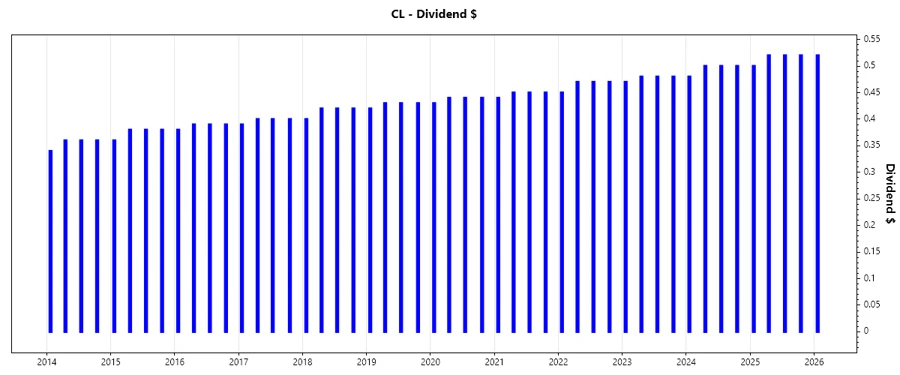

📈 Dividend History

A robust dividend history is crucial in evaluating a company's commitment to returning value to shareholders. Colgate's continuation over 54 years reflects strong financial management.

| Year | Dividend per Share (USD) |

|---|---|

| 2026 | 0.52 |

| 2025 | 2.06 |

| 2024 | 1.98 |

| 2023 | 1.91 |

| 2022 | 1.86 |

📉 Dividend Growth

Monitoring dividend growth is essential for assessing future capital returns. With modest growth rates of 3.42% over 3 years and 2.98% over 5 years, the consistency parallels the company's long-term resilience.

| Time | Growth |

|---|---|

| 3 years | 3.42% |

| 5 years | 2.98% |

The average dividend growth is 2.98% over 5 years. This shows moderate but steady dividend growth.

Payout Ratio

Payout ratios elucidate how much of the company's earnings and free cash flow are directed towards dividends. The EPS-based payout stands at 60.80%, while free cash flow supports coverage at 51.23%.

| Key figure | Ratio |

|---|---|

| EPS-based | 60.80% |

| Free cash flow-based | 51.23% |

These payout ratios denote a sustainable dividend policy, although improvements in earnings growth could reinforce stability.

🗣️ Cashflow & Capital Efficiency

Evaluating cash flows and capital efficiency metrics reveals the company's ability to sustain operations, fund growth, and return capital through dividends.

| Metric | 2024 | 2023 | 2022 |

|---|---|---|---|

| Free Cash Flow Yield | 4.77% | 4.61% | 2.82% |

| Earnings Yield | 3.89% | 3.49% | 2.71% |

| CAPEX to Operating Cash Flow | 14.26% | 18.83% | 27.23% |

| Stock-based Compensation to Revenue | 0.68% | 0.63% | 0.70% |

| Free Cash Flow / Operating Cash Flow Ratio | 86.34% | 81.17% | 72.77% |

Analysis indicates strong capital efficiency, though higher CAPEX ratios merit attention to sustain long-term efficiencies.

Balance Sheet & Leverage Analysis

An examination of Colgate's balance sheet outlines the financial leverage and liquidity, ensuring capacity to cover obligations and fund investments.

| Ratio | 2024 | 2023 | 2022 |

|---|---|---|---|

| Debt-to-Equity | 40.15 | 14.88 | 23.12 |

| Debt-to-Assets | 53.05% | 55.29% | 58.93% |

| Debt-to-Capital | 97.57% | 93.70% | 95.85% |

| Net Debt to EBITDA | 1.53 | 1.91 | 2.52 |

| Current Ratio | 0.92 | 1.11 | 1.28 |

| Quick Ratio | 0.58 | 0.71 | 0.76 |

| Financial Leverage | 75.69 | 26.92 | 39.23 |

The data indicates robust leverage standings with noteworthy debt reductions over recent years, ensuring safeguards against fiscal vulnerabilities.

Fundamental Strength & Profitability

Fundamentals provide insight into operational efficiency and profit generation potential, critical for sustaining dividend policies.

| Metric | 2024 | 2023 | 2022 |

|---|---|---|---|

| Return on Equity | 13.63% | 3.78% | 4.45% |

| Return on Assets | 18.00% | 14.03% | 11.35% |

| Net Margin | 14.37% | 11.82% | 9.93% |

| EBIT Margin | 21.13% | 18.91% | 15.73% |

| EBITDA Margin | 24.14% | 21.82% | 18.77% |

| Gross Margin | 60.23% | 57.82% | 56.49% |

| Research & Development to Revenue | 1.77% | 1.76% | 1.78% |

These metrics signal consistent profit margins, supported by strategic research and development expenditures.

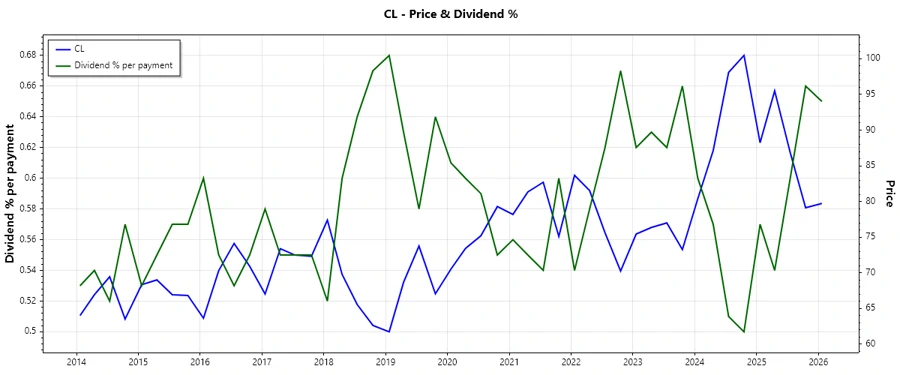

✅ Price Development

📈 Dividend Scoring System

| Criterion | Score | Rating |

|---|---|---|

| Dividend yield | 4 | |

| Dividend Stability | 5 | |

| Dividend growth | 3 | |

| Payout ratio | 4 | |

| Financial stability | 4 | |

| Dividend continuity | 5 | |

| Cashflow Coverage | 4 | |

| Balance Sheet Quality | 4 |

Overall Score: 33/40

🔍 Rating

Overall, Colgate-Palmolive maintains a formidable dividend presence, suitable for investors valuing income stability more than aggressive growth. Despite moderate payout flexibility, its resilience in adverse times underwrites a solid HOLD rating.