February 26, 2026 a 07:46 am

BBY: Dividend Analysis - Best Buy Co., Inc.

Best Buy Co., Inc. has consistently impressed with a strong dividend profile. With a solid dividend yield and a long history of payouts, it stands out among its peers in the retail industry. However, investors should take note of certain financial metrics which suggest areas of cautious optimism. Here's a detailed analysis of Best Buy's dividend performance and financial health.

📊 Overview

Best Buy operates within the retail sector, boasting a dividend yield of 5.23%, which is attractive in today's market. The company, a stalwart in dividends with a 23-year history of payments, last cut or suspended its payout in 2017. This positions Best Buy as a potential investment for income-focused portfolios.

| Metric | Detail |

|---|---|

| Sector | Retail |

| Dividend yield | 5.23 % |

| Current dividend per share | 3.75 USD |

| Dividend history | 23 years |

| Last cut or suspension | 2017 |

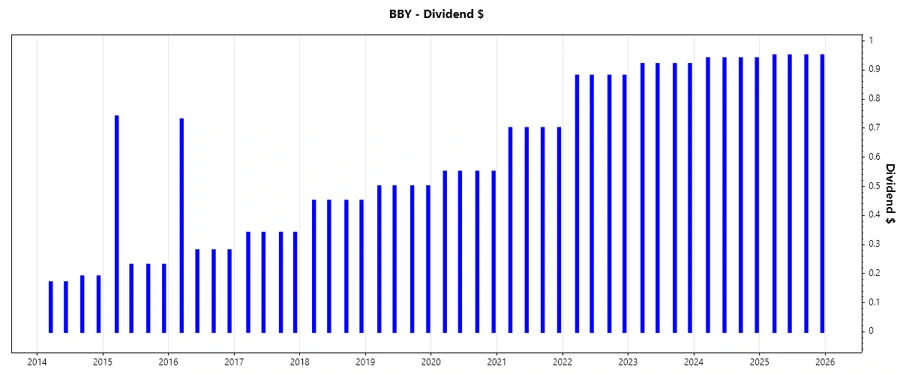

📉 Dividend History

Best Buy has demonstrated a history of stable and increasing dividends, reflecting its commitment to shareholder returns. This stability is crucial for investors looking for reliable income streams, mitigating risks in more volatile sectors.

| Year | Dividend Per Share (USD) |

|---|---|

| 2025 | 3.80 |

| 2024 | 3.76 |

| 2023 | 3.68 |

| 2022 | 3.52 |

| 2021 | 2.80 |

📈 Dividend Growth

The dividends have exhibited growth over the years, marking an average increase. This incremental growth is an indication of stable financial conditions within Best Buy.

| Time | Growth |

|---|---|

| 3 years | 2.58 % |

| 5 years | 11.55 % |

The average dividend growth is 11.55% over 5 years. This shows moderate but steady dividend growth.

🗣️ Payout Ratio

The payout ratios are vital for assessing the sustainability of dividend payments. A high payout ratio might indicate that a company is overly reliant on its earnings to maintain dividends.

| Key figure | Ratio |

|---|---|

| EPS-based | 122.50 % |

| Free cash flow-based | 52.04 % |

An EPS payout ratio of 122.50% suggests caution as it exceeds 100%, indicating dividends exceed net income. However, the FCF payout at 52.04% suggests some coverage through cash flow, though slightly above ideal levels.

✅ Cashflow & Capital Efficiency

Analyzing cash flow and capital efficiency helps to reveal the company's ability to generate cash and manage its capital expenditures effectively, ensuring long-term sustainability. The following data illustrates Best Buy's recent financial metrics, highlighting its strengths and areas for improvement.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Free Cash Flow Yield | 4.67% | 4.10% | 7.53% |

| Earnings Yield | 7.41% | 7.53% | 5.02% |

| CAPEX to Operating Cash Flow | 50.99% | 54.08% | 33.65% |

| Stock-based Compensation to Revenue | 0.30% | 0.33% | 0.33% |

| Free Cash Flow / Operating Cash Flow Ratio | 49.01% | 45.92% | 66.35% |

The cash flow stability indicated by a favorable free cash flow yield suggests that Best Buy has a robust capacity to manage dividends effectively while maintaining efficient capital expenditure levels.

🔍 Balance Sheet & Leverage Analysis

Strong balance sheet management and leverage efficiency are indicative of a company’s financial stability and ability to withstand market fluctuations. Here, Best Buy illustrates some variability in its leverage metrics.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Debt-to-Equity | 142.33% | 130.43% | 144.34% |

| Debt-to-Assets | 25.17% | 26.61% | 27.42% |

| Debt-to-Capital | 58.73% | 56.60% | 59.07% |

| Net Debt to EBITDA | 0.77 | 0.98 | 1.12 |

| Current Ratio | 0.98 | 1.00 | 1.03 |

| Quick Ratio | 0.41 | 0.37 | 0.39 |

| Financial Leverage | 5.65 | 4.90 | 5.26 |

The metrics reveal a consistent leverage strategy, though with a slightly elevated debt-to-equity ratio, which warrants a watchful eye on future borrowings.

🔥 Fundamental Strength & Profitability

Examining the fundamental strengths and profitability metrics of Best Buy provides insight into the company's ability to generate returns and maintain a competitive edge within the sector.

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Return on Equity | 50.77% | 40.65% | 33.01% |

| Return on Assets | 8.98% | 8.29% | 6.27% |

| Net Margin | 3.06% | 2.86% | 2.23% |

| EBIT Margin | 3.94% | 3.85% | 3.24% |

| EBITDA Margin | 5.92% | 5.97% | 5.33% |

| Gross Margin | 21.41% | 22.10% | 22.60% |

| R&D to Revenue | 0% | 0% | 0% |

Despite fluctuations, Best Buy maintains a robust ROE, suggesting solid profitability and an efficient use of equity capital, though low R&D investment may impact future innovation.

📷 Price Development

✨ Dividend Scoring System

| Criteria | Comment | Score |

|---|---|---|

| Dividend yield | Strong yield above industry average | |

| Dividend Stability | Consistent payout history | |

| Dividend growth | Moderate long-term growth | |

| Payout ratio | High EPS payout raises sustainability concerns | |

| Financial stability | Manageable debt, robust financial health | |

| Dividend continuity | No cuts since 2017 | |

| Cashflow Coverage | Reasonable coverage of dividends | |

| Balance Sheet Quality | Strong leverage ratios, careful management |

Overall Score: 57 out of 80

🔍 Rating

Overall, Best Buy Co., Inc. presents a compelling dividend investment profile with a strong yield and solid history of payouts. However, the elevated EPS payout ratio and moderate growth warrant a cautious but optimistic outlook. While well-positioned in terms of financial health and operational efficiency, future attention should focus on maintaining sustainability amidst evolving market conditions. Recommended as a “Hold” for income-seeking investors with a focus on stability and consistent returns.